14(1)The APR for a lease is calculated in accordance with the following formula:

APR = M Ă— I Ă— 100

where

APR is the annual percentage rate;

M is the number of payment periods in a year under the lease; and

I is the periodic interest rate, as determined under subsection (2).

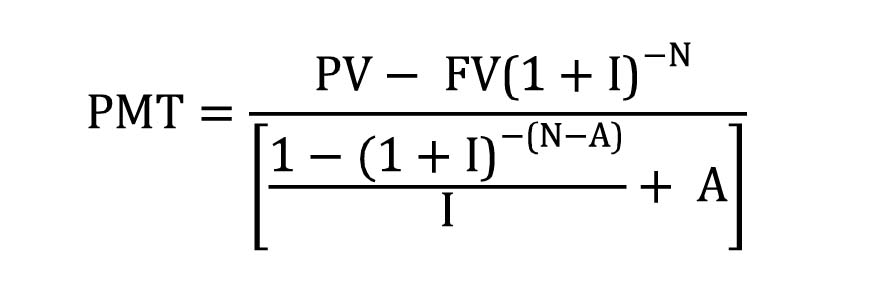

14(2)The periodic interest rate is the value of “I” in the following formula:

where

PMTis the amount of each periodic payment under the lease;

Ais the number of periodic payments under the lease that are made at or before the beginning of the term;

PVis the capitalized amount;

FVis the amount of the assumed residual payment;

Iis the periodic interest rate; and

Nis the number of payment periods under the lease.

14(3)For the purposes of calculating the APR and implicit finance charge for a lease,

(a)

an amount payable by the lessee in respect of a tax is regarded as a payment only if an amount in respect of the tax was treated as an advance in calculating the capitalized amount, and

(b)

a charge payable by the lessee is regarded as an advance only if an equivalent charge would be payable by a cash customer.

14(4)If there is any irregularity in the amount or timing of payments required during the term, the equation in subsection (2) shall be modified as necessary to calculate the value of “I” in accordance with actuarial principles.

14(5)For the purposes of calculating the APR and implicit finance charge for a lease referred to in paragraph (b) of the definition “lease” in subsection 1(1) of the Act, the term of the lease is assumed to be one year.

14(1)The APR for a lease is calculated in accordance with the following formula:

APR = M Ă— I Ă— 100

where

APR is the annual percentage rate;

M is the number of payment periods in a year under the lease; and

I is the periodic interest rate, as determined under subsection (2).

14(2)The periodic interest rate is the value of “I” in the following formula:

where

PMTis the amount of each periodic payment under the lease;

Ais the number of periodic payments under the lease that are made at or before the beginning of the term;

PVis the capitalized amount;

FVis the amount of the assumed residual payment;

Iis the periodic interest rate; and

Nis the number of payment periods under the lease.

14(3)For the purposes of calculating the APR and implicit finance charge for a lease,

(a)

an amount payable by the lessee in respect of a tax is regarded as a payment only if an amount in respect of the tax was treated as an advance in calculating the capitalized amount, and

(b)

a charge payable by the lessee is regarded as an advance only if an equivalent charge would be payable by a cash customer.

14(4)If there is any irregularity in the amount or timing of payments required during the term, the equation in subsection (2) shall be modified as necessary to calculate the value of “I” in accordance with actuarial principles.

14(5)For the purposes of calculating the APR and implicit finance charge for a lease referred to in paragraph (b) of the definition “lease” in subsection 1(1) of the Act, the term of the lease is assumed to be one year.